Thriving economies need capital. Yet, this is one of the components that poor countries lack the most. It almost goes without saying. Capital is like the grease that enables the economic engine to run. It funds innovations that create employment and provide taxes for governments to do their work more effectively. As such, the notion that wealthy nations should pump poor countries with capital is understandable.

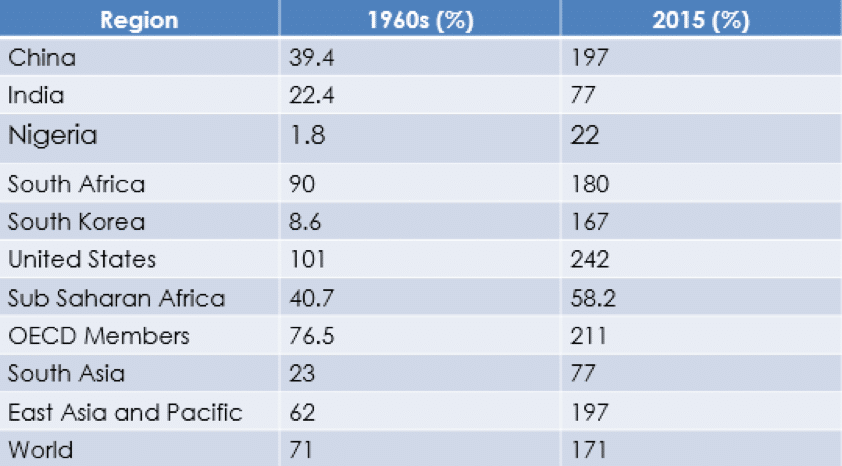

Consider the difference in capital and credit in OECD countries (a group of 35 of the world’s wealthiest countries) versus sub Saharan African countries. Domestic credit to GDP ratio—the amount of domestic credit available in the system compared to the gross domestic product of the country—is an indicator of a country’s economic strength. In 2015, domestic credit to GDP ratio in OECD countries was 211%. There was more than twice as much credit available in the system than GDP in those countries. For sub Saharan Africa, it was 58%. Consider that in 2015, the GDP of OECD countries was just over $52 trillion, while that of sub Saharan Africa was less than $2 trillion. This therefore means that the available credit in OECD countries was more than $109 trillion while sub Saharan Africa’s private credit is around $1.2 trillion. Poor countries need more credit; they need more capital.

Domestic Credit to GDP Ratio, Selected Regions

The question, however, is how should capital be deployed to poor countries? What distribution mechanism should be used?

The stock market is not the answer

The ability to trade in shares of companies is one of the hallmarks of prosperous countries. Companies get created, they show promise, and go public. This sequence of events is a tried and true method of raising capital and “greasing” the economy. In 2015, for instance, the United States’ stock market mobilized approximately $20 trillion worth of capital, while Japan and the United Kingdom mobilized around $3 trillion and $2.7 trillion, respectively. These are all prosperous countries. It is reasonable, therefore to surmise that poor countries should develop their stock markets so that they can also attract capital and grease their economies. Unfortunately, doing so would have devastating impacts on companies in poor countries.

First, the regulatory demands of the stock market are antithetical to the kinds of innovations and businesses that poor countries must cultivate in order to prosper. Chief of these regulatory requirements is the need to report progress every quarter. If managers are not able to show progress, their stock price is punished. However, emerging market investors in poor countries need to invest in market-creating innovations which typically take longer to come to fruition. The expectation that these innovations will reap rewards in a few short months, especially at their onset, is not realistic, and is quite counterproductive.

Second, focusing on creating stock markets without first creating markets is akin to putting the cart before the horse. And when that happens, neither the cart nor the horse moves. The stock market is nothing more than a distribution mechanism to get capital to flow to productive enterprise. It does not create productive enterprise. If there isn’t already a culture and a foundation of innovation that fuels productive enterprise, we will effectively create stock markets without markets.

Creating productive enterprise through market-creating innovations

As I’ve written before, market-creating innovations target nonconsumers—the segment of the population who would benefit by owning or using a product but cannot due to the product’s cost, time, or the the expertise needed to use it. These innovations transform complex and expensive products into simple and more affordable products, making them accessible to a wider segment of the population.

In poorer societies, nonconsumers typically make up the majority, thus innovators must hire many people to make, distribute, sell, and service their market-creating innovations. As such, from a job creation standpoint, it is net positive. Also, these innovations make society as a whole significantly more productive. But perhaps of more importance is their impact on economic and societal development, as demonstrated by Henry Ford’s Model T car.

Unlike existing cars on the market, Henry Ford manufactured a car that was inexpensive enough for an American with a modest income to purchase. He also made the car easier to drive so that owners would not have to hire a driver or need special expertise. In doing so, cars that had formerly been exclusive to the wealthy were now accessible to a far greater population, resulting in massive job creation and widespread changes to the country. Among these changes included the ability of long-distance travel, living in suburbs, going out to restaurants near or far, gas stations, and gasoline taxes (which helped build many of the United States’ roads). In the same way, poorer countries can create job opportunities and build markets from the ground up by investing in market-creating innovations.

Build the markets, the stocks will come

One of the biggest problems in the world of economic development is that development and investment professionals “know” the answer to the development conundrum. All we need do is “look” at what rich countries have, hold down “Ctrl+C” to copy what we believe the answer is, and then hold “Ctrl+P” and paste the answer in poor countries. It is a compelling strategy. But it is also a flawed one. Attempting to replicate the methods used by wealthy countries fails to recognize those countries’ unique circumstances and the context in which those countries created wealth from the start. While we can learn from them, it would be a mistake to assume there is a one-size-fits-all approach that can be applied to all countries looking to escape poverty.

If we build markets by focusing on investments that target market-creating innovations, the stock market will swiftly follow. Let us build markets first.

For more, see:

This activity is the most important component of your nation’s GDP