For more, see:

How health plan innovation can cure the Affordable Care Act

Obamacare, we have a problem

Reducing the cost burden on the insured

EXECUTIVE SUMMARY

Throughout history, disruptive innovations have repeatedly, and often predictably, transformed entire industries through the introduction of affordable and accessible products and services. Personal computers, automobiles, mobile phones, airplanes, and email are disruptive innovations that have permanently changed the world around us by making previously expensive and complicated products increasingly available to larger groups of people. Today, with health care costs spiraling ever higher, the U.S. is in a health care crisis—and in dire need of disruptive innovations that could make quality care more affordable and accessible.

In 2010, the passage of the Patient Protection and Affordable Care Act (ACA) dramatically altered the U.S. health care industry. It remains one of the most controversial pieces of legislation passed in decades. In October 2013, significant provisions of the act will be implemented and the health care ecosystem will once again shift to accommodate new regulation and infrastructure.

A complicated policy with over 955 pages and countless congressional revisions, it is naïve to claim that the ACA is a wholly good or bad policy. With such complexity and nuance, sweeping statements of political or economic ideology do little to address the reality at hand. Provisions of the law are now being implemented, and it is essential that policymakers, medical practitioners, and innovators alike consider where opportunities for disruptive innovation reside. It is also essential to consider which provisions of the law might inhibit disruptive innovation and focus reform efforts on those provisions.

It is through leveraging opportunities to innovate and disrupt within the health care industry that we will move closer to the one goal almost everyone agrees upon: making health care more affordable and more accessible to all people. It is for this purpose that we have completed this study: to analyze the ACA through the lens of disruptive innovation and provide insight into the specific provisions that offer the greatest potential for positive change and disruption—as well as to identify which provisions may dis-incentivize such change and disruption. Doing so allows us to better understand and leverage new and potential opportunities that increase accessibility, decrease costs, and improve overall quality of care.

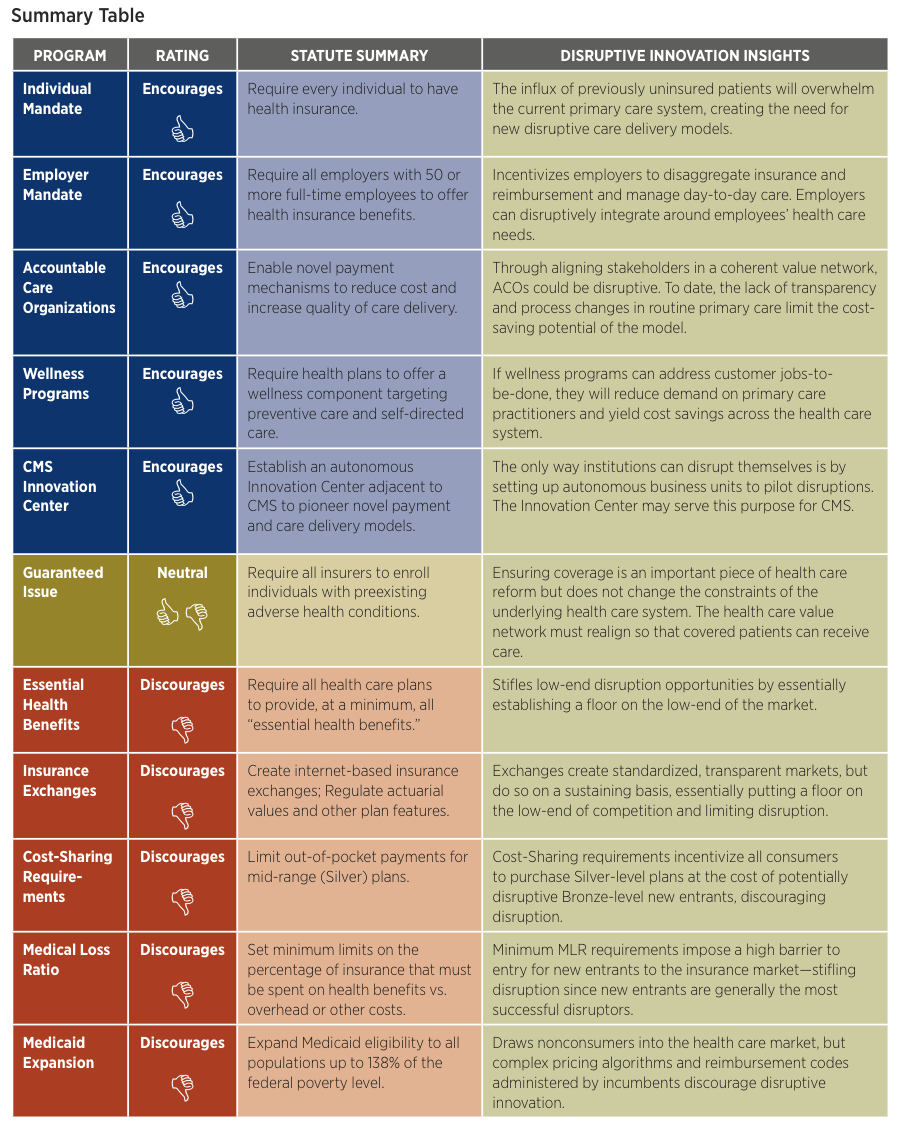

Ways in which the ACA Encourages Disruptive Innovation

Looking at the ACA through the lenses of disruptive innovation, we see several aspects of the law that open the door for disruption. These include the following items:

- Individual Mandate

- Employer Mandate

- Accountable Care Organizations (ACOs)

- Wellness Programs

- CMS Innovation Center

The Individual Mandate, which essentially requires all Americans to maintain health insurance, will bring a large population of currently uninsured individuals into the primary care system. We anticipate that this will increase demand on an already-burdened system and create space for new care delivery models that leverage less-credentialed practitioners to deliver care for more routine health concerns. Such business models are present already in retail health clinics that allow nurse practitioners to treat patients in convenient locations such as neighborhood pharmacies. This innovative approach both relieves the burden on traditional clinics and makes quality care more affordable and accessible for thousands of patients.

The Employer Mandate, which requires all employers with 50 or more full-time-equivalent employees to offer health insurance benefits, increases the financial demands on employers to provide health care coverage for their employees. As employers look to manage expanding health care costs, there will be greater demand for alternate models of health insurance. Some employers will be more proactive in providing their own health care services, looking only to insurance companies for catastrophic care coverage or no coverage at all. This could facilitate a substantial disaggregation in the insurance industry and open opportunities for new and disruptive entrants to provide health services to employers as well as for entrants in the insurance industry to provide new forms of coverage.

Accountable Care Organizations (ACOs), which are expected to proliferate under the ACA, were created with the goal of aligning the conflicting interests in the care delivery value network. By making providers responsible for the cost and quality of the care they deliver, these programs are architected to improve health care quality and financially incentivize providers and payors to keep patients healthy, rather than simply treat them when they are sick. If executed successfully, such a system would yield a coherent value network that could enable disruptive business models in care delivery to flourish.

The ACA’s provisions that support the development of Wellness Programs yield another exciting possibility for innovation. These provisions require health plans to offer wellness-focused components targeting preventive and self-directed care. Few argue against the notion that health care costs would drop substantially if we could prevent more chronic diseases and acute illnesses. To date, wellness programs have struggled to produce material cost savings, as the patients who need them most often don’t utilize them until after they are ill. Innovative companies that create products and/or services that improve patient wellness by successfully addressing patients’ existing “jobs-to-be-done” will be poised for explosive growth that could disrupt much of the existing system.

Another provision of the ACA creates the CMS Innovation Center, an organization charged with pioneering novel payment and care delivery models while operating outside the conventional infrastructure of the Centers for Medicare and Medicaid Services. One of the key tenets of the theories of disruptive innovation is that it is extraordinarily difficult for an organization to disrupt itself. Time and time again, existing business models, profit targets, and entrenched interests squash disruptive innovations because those innovations often require different models, profit margins, and priorities to succeed. The only way for organizations to disrupt themselves is to set up a separate entity, free of the demands of the existing business, to identify new markets and disruptive paths. If permitted to operate with sufficient independence, the Innovation Center could be a critical source of disruptive innovations for CMS.

Ways in which the ACA Discourages Disruptive Innovation

Just as there are some ACA provisions that create opportunity for disruptive innovation, there are also portions of the ACA that will likely inhibit disruptive innovation. While these provisions of the ACA might discourage entrepreneurs and innovators, we identify them because they are critical areas for policymakers and other stakeholders to focus their reform efforts. Provisions of the ACA that will likely inhibit disruptive innovation include the following items:

- Essential Health Benefits

- Insurance Exchanges

- Cost-Sharing

- Medical Loss Ratio

- Medicaid Expansion

The Essential Health Benefits created by the ACA limit disruptive innovation by placing requirements on the services that must be covered by any health insurance plan. This mandated level of coverage exceeds what customers need in many cases and will make it more difficult for innovators to bring truly low-end disruptive health insurance plan designs to market.

Disruptive innovation is further limited by the Insurance Exchanges, online marketplaces that will allow individuals and small companies to compare health insurance alternatives. Although these exchanges will improve transparency in terms of coverage options and pricing, the ACA’s tight restrictions around coverage requirements essentially put a floor on the low end of coverage, thus limiting opportunities for entrants to provide different types of coverage and methods of care delivery.

The Cost-Sharing requirement imposed by the ACA—although created with the good intention of making quality health insurance affordable to low-income individuals and families— actually discourages disruptive innovation in ways similar to the Essential Health Benefits and Insurance Exchange provisions. By funneling low-income consumers into Silver-level plans via government subsidies, this provision will reinforce status quo plan designs and artificially constrain demand at the low end of the market (i.e., Bronze-level plans).

Enacted to prevent insurance companies from over-charging and/or not reimbursing customers for medical care, the Medical Loss Ratio provisions require insurers to justify rate increases and spend a minimum of 80 percent of premiums on health care. As new, disruptive entrants are likely unable to immediately replicate incumbent payors’ large membership bases and economies of scale, the barriers to entry in terms of spending requirements are daunting, if not insurmountable.

Lastly, covering increasing numbers of patients at the low-end of the market through Medicaid Expansion limits the size of the market available to potential disruptive innovators, as millions of would-be customers will receive traditional health insurance from the government. Complex pricing mechanisms driven by CMS’s pricing algorithms also constrain disruptors by limiting reimbursement options for innovative care delivery processes and products.

It is essential to note that the common thread amongst these provisions is that they will not transform health care on their own. Although some of the provisions of the ACA may open doors for disruptive innovation, the onus rests upon the health care sector—existing players and new innovators alike—to seize the disruption opportunities and create products and services that make health care more affordable and accessible. Great opportunities exist to provide care to the millions of patients now entering the primary care system. Where policymakers look to improve upon the ACA’s provisions, we encourage them to focus their efforts on portions of the ACA that inhibit disruptive innovation, as such provisions will maintain higher prices and limit the accessibility of quality care within the sector.