EXECUTIVE SUMMARY

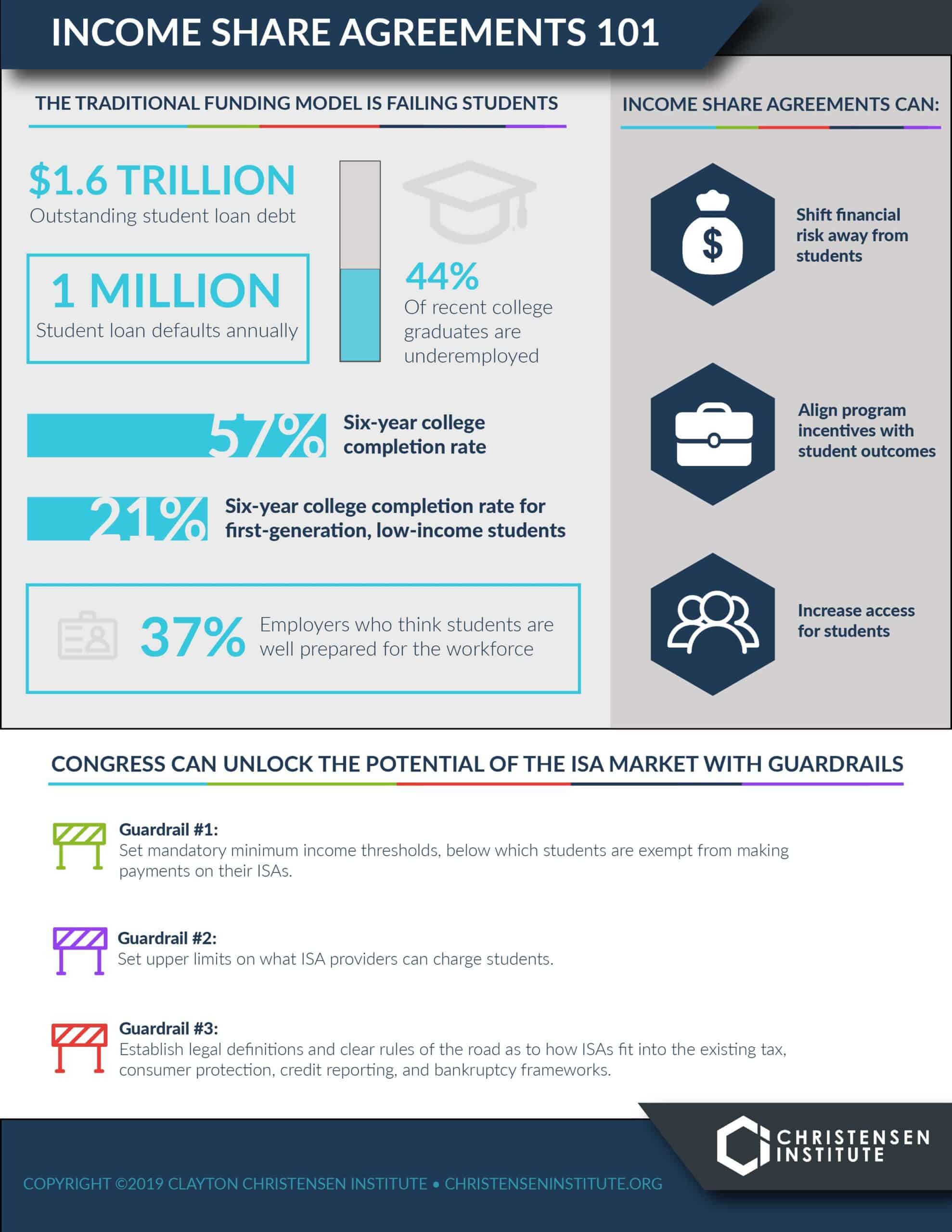

With one million defaults on student loans every year, and $1.6 trillion in outstanding student debt, it’s clear the U.S. is in desperate need of innovative funding models in higher education. Income Share Agreements, or ISAs, stand to provide a promising alternative to high-risk student loans, as they better align the interests of students, schools, and lenders.

In an ISA, students pay no tuition upfront, only repaying the education provider once employed—in essence, funding today’s educational opportunities for a fixed percentage of tomorrow’s income, within a set window of time. In other words, an ISA is an equity investment, whereas a student loan is a debt burden.

ISAs have the potential to both protect students from paying for educational experiences that don’t create value for them in the labor market, shifting the risk of poor workforce outcomes away from students, and to produce better outcomes by putting that risk on schools and giving them skin in the game. After all, education providers are more likely to help students graduate and get good jobs if that’s how the schools get paid. Aligning incentives between schools, capital providers, and students could redefine the value of college.

ISAs thus serve as a viable choice for students seeking to finance their education, and in many cases, increase access to higher education by helping students afford programs not eligible for federal financial aid.

Despite the potential of the ISA model, a lack of regulatory clarity has limited its adoption. To reach that potential, the ISA market needs guardrails that both protect students and encourage investment in the space. The recently proposed ISA Student Protection Act of 2019 gives policymakers an opportunity to establish clear rules of the road for the ISA market.

- First, the ISA market should be bounded by a minimum income threshold, limiting downside risk for students in cases of unemployment or underemployment. The current bill’s proposal to index this threshold to the Federal Poverty Line is a strong first step.

- Second, the ISA market needs payment caps to keep students from paying exorbitant amounts. The current bill limits both the percentage of income and a value known as the “commitment factor,” striking a good balance of protecting students while giving ISA providers room to experiment with different types of caps.

- Third, the ISA market needs greater transparency to help students make informed decisions when considering ISAs, and to help ISA providers understand the legal framework in which they operate. The current bill offers a legal definition of ISAs, and clarity around their treatment under tax and consumer protection laws.

With clearer rules of the road, ISAs will be better positioned to address the needs of those for whom existing solutions aren’t working. We welcome ISAs as an innovative addition to the higher education financing toolbox, and encourage Congress to do the same.