What will be profitable in the future? This question vexes analysts and entrepreneurs, and few answer it correctly. Three out of four venture-backed firms do not result in return for investors, and just one company in eight manages to consistently grow with above-average shareholder returns. Firms that successfully identify where future profit will lie are successful, and those that do not ultimately fail.

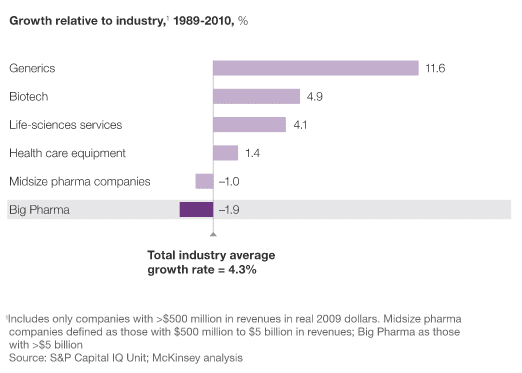

Understanding what will be profitable is central to resolving the current crisis facing the U.S. pharmaceutical industry. Expiring patents, regulatory burdens, and lack of new blockbuster drugs are constricting growth and shrinking margins. Firms that understand the process of commoditization and decommoditization will be able to successfully navigate this predicament by “skating to where the puck will be” and capturing future profits while simultaneously utilizing disruptive innovations to make health care more affordable and accessible. Firms that do not understand this process will likely invest in the wrong areas, outsource critical competencies, and ultimately cede the market to more adept competitors.

Will everything be commoditized?

A commodity is a product that is undifferentiable from other products and hence competes solely on the basis of price. For many people, milk, eggs, and notebook paper are commodities; price is the only deciding factor for most people when they purchase any of these items. Pharmaceutical company products are especially susceptible to commoditization: when a patent expires, a drug goes from proprietary profitable product to undifferentiable unprofitable commodity literally overnight. Many people believe that any product or innovation, no matter how spectacular, will eventually be commoditized and profits will disappear.

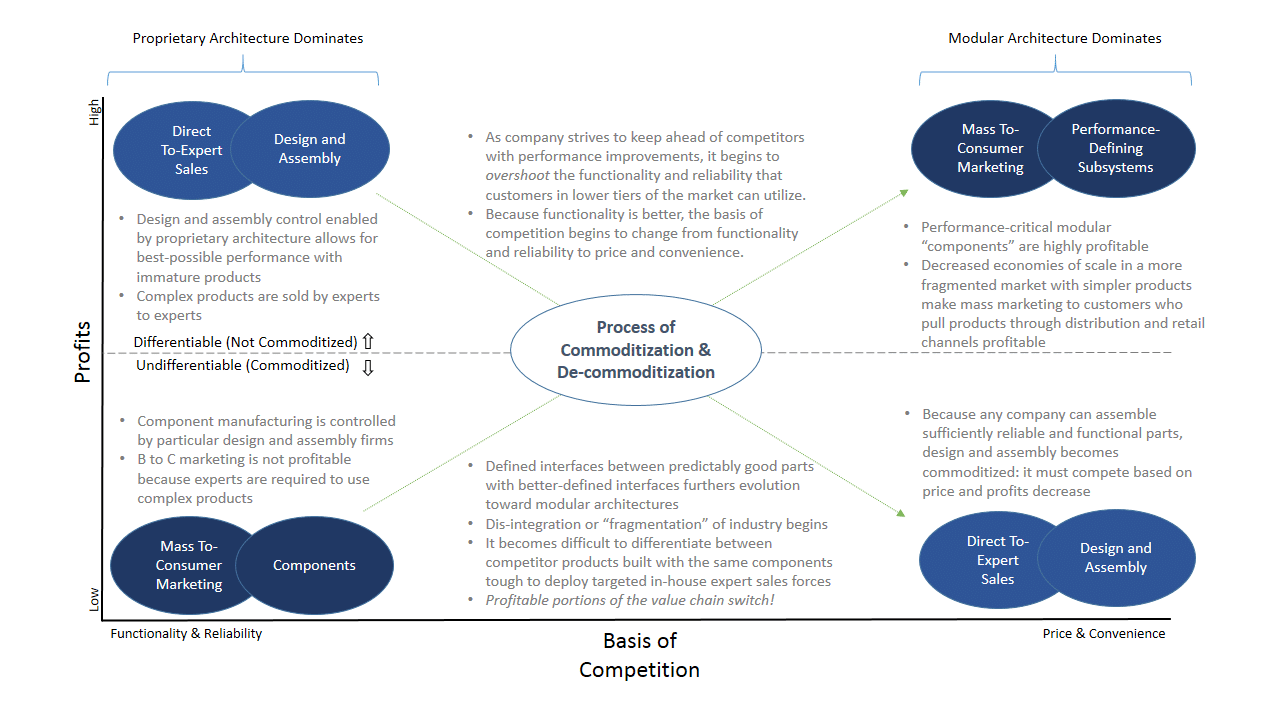

Fortunately, this view is overly simplistic. The process of commoditization and decommoditization within a value chain is predictable, and even as portions of the value chain become commoditized companies can capture profits with forward-looking strategic planning and execution. While profitable portions of a business’s value chain eventually become commoditized as modular architectures gain advantage, portions that were previously not profitable such as critical components or subsystems become profitable, as detailed in the chart below (click to enlarge).

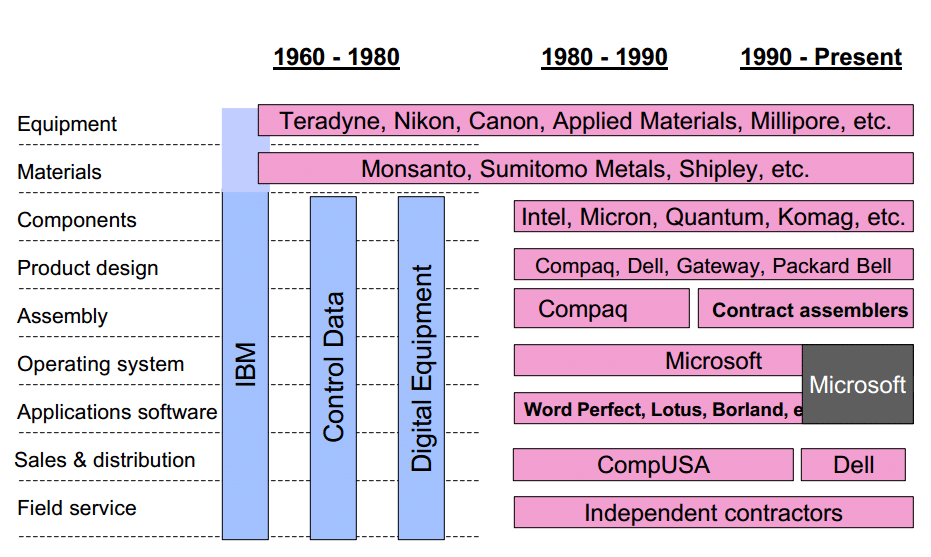

Commoditization and Decommoditization in the Computer Industry

This commoditization-decommoditization process has played out in every field. The computer industry, illustrated below, shows how large, proprietary systems yielded to modular architectures controlled by many different firms. Control Data and Digital Equipment on longer exist. IBM, however, established interoperability standards and set up separate business units that could profit under modular architectures and take advantage of the commoditization of design and assembly and decommoditization of other portions of the value chain, and so they survived.

Pharmaceutical Industry Modularization and Fragmentation

We could draw a similar chart for the pharmaceutical industry. “Big Pharma” companies historically controlled every aspect of drug creation from discovery to development to trials to marketing. As in most industries, proprietary technologies fueled R&D pipelines, familiarity with regulations and procedures aided drug approval, and expert salespeople employed by pharma companies sold directly to doctors.

In recent years, technological advances, patent expirations, and regulatory changes have started the process of design and assembly commoditization. Computer simulations, advances in small molecule understanding and development, rapid and inexpensive genomic sequencing, and other innovations have opened up discovery, research, and development to small firms. As patents expire, proprietary molecules are becoming commoditized. Direct-to-consumer marketing and readily available online drug information is decreasing the value of highly trained sales representatives. The market is fragmenting, or becoming modular.

In this precarious situation, financial and industry analysts are clamoring for large pharmaceutical companies to focus on the areas that have been profitable in the past – therapeutics via incremental improvements of existing treatments, high-cost marketing campaigns, and increased focus on traditional ‘core competencies’ while outsourcing other fixed costs. Businesses that follow these recommendations will find themselves trapped by their past successes, stuck in the rapidly commoditizing business of ‘design and assembly.’ Indeed, Kenneth Getz of Tufts University has found that, despite some successes, many outsourcing operations are poorly executed and do not deliver on their profitability promises. Large pharmaceutical firms stuck in the past will become little more than portfolio managers who bring together the people who are actually capturing profit in the new modular system.

Skating to where the puck will be

To avoid this scenario, pharmaceutical companies must, as hockey great Wayne Gretzky said, “Skate to where the puck will be.” Here are three ways pharma companies can look forward and capture future value:

- Focus on performance-defining subsystems rather than historically profitable competencies. Firms should ask “what system is not good enough” and focus strategy around the answer. Diagnostics, for example, is one subsystem that is often not good enough to enable precision medicine. Precision diagnostics can enable profitable, effective targeted treatments such as Herceptin for breast cancer which targets cancers caused by overexpression of the HER2 protein. Yet some big companies have already spun off their diagnostics divisions because, in the past, therapeutics was much more profitable than diagnostics. In the future, however, diagnostics will be a performance-defining subsystem that unlocks the door to successful therapies.

- Establish separate business units that can take advantage of a fragmented or modular industry. In a modular world, lower profit margins and differing sales strategies virtually prohibit large proprietary firms from competing with “the zero-person biotech company.” Minicomputer firms structured around making 60% margins on $500,000 sales could not operate with personal computer sales margins of 30% on $2,000. Consequently, most large mainframe and minicomputer companies failed. IBM, however, survived. Every time a new wave of disruption came along, it set up a completely separate business unit and allowed that unit to compete with and ultimately cannibalize its old business. Drug companies are in a similar position to large computer manufacturers: firms structured around high-margin blockbuster drugs cannot operate developing and selling lower-margin niche drugs. Like IBM, companies must establish independent, competitive business units. Johnson & Johnson follows a similar strategy now with their over 200 businesses. Other companies must follow suit if they are to survive.

- Re-integrate around systems that emphasize speed, responsiveness, and customization. In proprietary, integrated systems, improved functionality beats competitors. Patented blockbuster drugs fall into this category. When they go off-patent, pharma companies are tempted to ‘upgrade’ their functionality with incrementally improved molecules or multi-drug combinations. These sustaining innovations are not bad. However, in a world of modular manufacturing of generic drugs, real value lies in ensuring the fluidity (speed and responsiveness) and customization of the patient experience all the way from trial to treatment. Companies that can offer convenient, comprehensive targeted care solutions will ultimately beat those focused on getting patents for incrementally improved iterations of old blockbusters.

Commoditization and fragmentation is not the end of effective and profitable pharmaceuticals. Nonetheless, the following decade will continue to be one of great upheaval unless firms focus on capturing future, not past, profits.