Imagine if your auto insurance included coverage for gas. On its surface it may seem like a nice convenience, but in practice it would be messy. The documentation to track where, when, and how much gas you consumed would be cumbersome. The controls to ensure you weren’t pumping gas for your lawnmower or boat under your auto insurance policy would be complex. And the incentives this arrangement presented would be a problem—consumers wouldn’t care much about how much gas they used or at what price they bought it if it were all ‘covered’ by their insurance. As a result, auto insurance costs would likely spiral out of control.

It’s no wonder auto insurance policies don’t cover gas. Bundling a predictable, routine expense like gas with relatively random but catastrophic expenses resulting from accidents and crashes makes it very difficult to control costs and encourage the right behaviors. This is what we call the bundled insurance problem, and unfortunately health insurance suffers from this ailment.

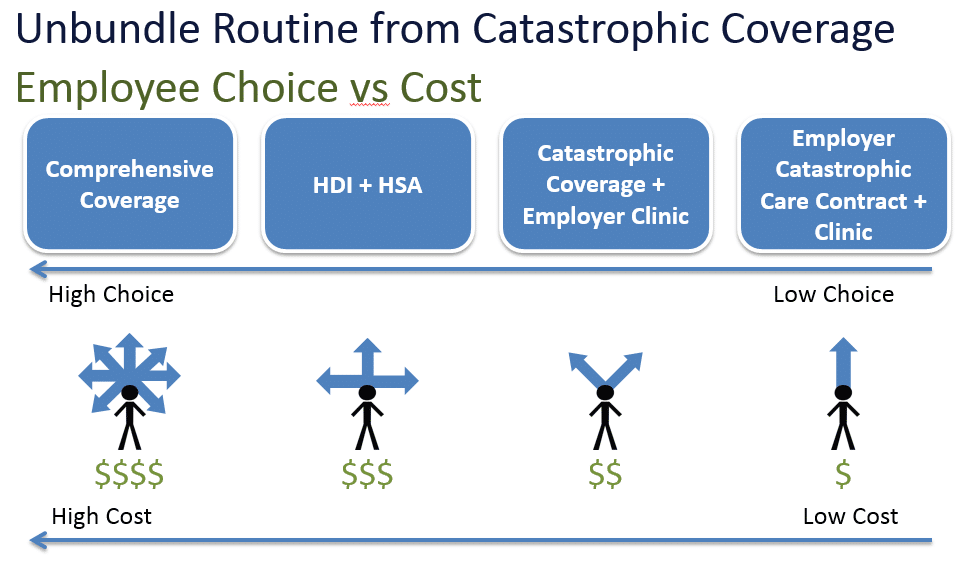

What can be done about the bundled insurance problem? There are no simple solutions, but for starters we think employers can make significant progress since they provide health insurance coverage for nearly 45% of insured Americans and have a significant incentive to keep their people healthy and manage health care costs. We propose a simplistic continuum that employers can use to move toward unbundling predictable consumption of health care from the truly random events that are insurable (see image below).

On the leftmost side of the model is comprehensive coverage. This is health insurance that allows patients to see nearly any provider they want, but comes at a high cost. Many PPO plans fit this description. Employers tend to offer these plans in hopes of retaining key talent. We think it’s worth asking whether compensating employees with more cash would have a greater retention effect than buying them expensive bundled insurance plans that allow nearly unlimited choices.

One step to the right is a high-deductible insurance plan coupled with a health savings account. Over two-thirds of employers with >1,000 employees in the US are now offering at least one of these benefit plans currently. These plans maintain significant choice of provider, but require significant out of pocket costs in the form of a high deductible before insurance reimbursement kicks in for non-preventive care. This out of pocket cost results in lower insurance premiums and does a better job than comprehensive coverage in unbundling the predictable, routine costs from the random, catastrophic costs. These plans also typically reign in health care cost inflation. However, in these plans the insurer still sets the provider network and governs how the patient navigates that network.

A more aggressive step toward unbundling routine from catastrophic coverage is by employers taking ownership of routine care and buying catastrophic coverage plans for expensive, catastrophic care. Kaiser began this way in the 1930s and 1940s when Henry Kaiser began owning and providing health care for his 30,000+ construction, ship yard, and steel mill employees. We’re seeing this more recently with companies like Pitney Bowes and many others. This approach significantly reduces patient choice of provider, but allows employers to deliver health coverage at lower cost and presumably higher quality. More recently, employer on-site clinic operators have emerged (e.g., QuadMed) to make getting into the health care delivery business even easier for employers.

Finally, we’re beginning to see signs that large employers may disrupt the health insurance business model entirely by contracting directly with hand-picked providers on a disease-by-disease basis and offering primary care services on-site. Wal-Mart’s centers of excellence program is evidence that large employers can develop the financial and clinical wherewithal to bypass payor networks entirely and get better care at the same or lower total cost on a population basis. As technology improves, we expect more large employers to contract directly with providers and bypass payors. Meanwhile, provision of routine care can be done in-house as a way to improve employers’ intelligence on their employee population’s health needs. This would dramatically restrict provider choice, but at potentially significant financial savings by completely unbundling routine from catastrophic care.

We realize this model only covers 45% of insured Americans, and that the government-payor situation is an entirely different problem that is not covered here. However, we are optimistic that if employers aggressively work to unbundle routine and catastrophic care they will be able to reduce their health care costs and enable improved physical and financial health for their employees.

The author acknowledges the contributions of Jeff Wheeler to this blog post.