The printing press eliminated copyists and created editors. Electricity killed the gas lamp and built an industry. The personal computer ended typing pools and opened entire sectors. The optimistic reading looks at cases like these and generalizes: every technology destroys some jobs and creates more than it destroys. Productivity rises, prices fall, demand expands, and net employment always ends up growing. At least that’s what the narrative says.

Then AI shows up, and the same question returns: Is this time different?

The question is wrong. The pattern of “what technology does to employment” never existed. In some periods, technology created jobs; in others, it destroyed them. The difference was never in the technology itself.

It’s in use. The same technology, deployed for different purposes, produces opposite effects on employment. Within the same sector, at the same moment, both directions can run in parallel. So, whether AI will create or destroy jobs is not a forecast about AI. It’s an observation about how AI is being used.

The operators’ turn

Consider telephone operators. In the early 20th century, telephony was one of the largest employers in the United States. By 1947, there were more than 350,000 operators connecting calls on manual switchboards. The sector grew for half a century because connecting people required people, and each new line created demand for more connections.

Then came automatic switching. By the 1980s, the profession had practically disappeared. It was the same industry, with the same underlying service, but two opposite employment trajectories as the underlying technology turned over. The sign flipped without the sector changing markets.

This isn’t an isolated case. James Bessen, at Boston University, studied two centuries of American data in textiles, steel, and automotive, and all three showed the same inverted-U pattern. Productivity rose the whole time, but employment grew for decades, peaked, and then collapsed. Textiles fell from 300,000 in 1958 to 16,000 in 2011. Steel went from 500,000 to 100,000. Productivity doesn’t decide employment. The use does.

Two directions

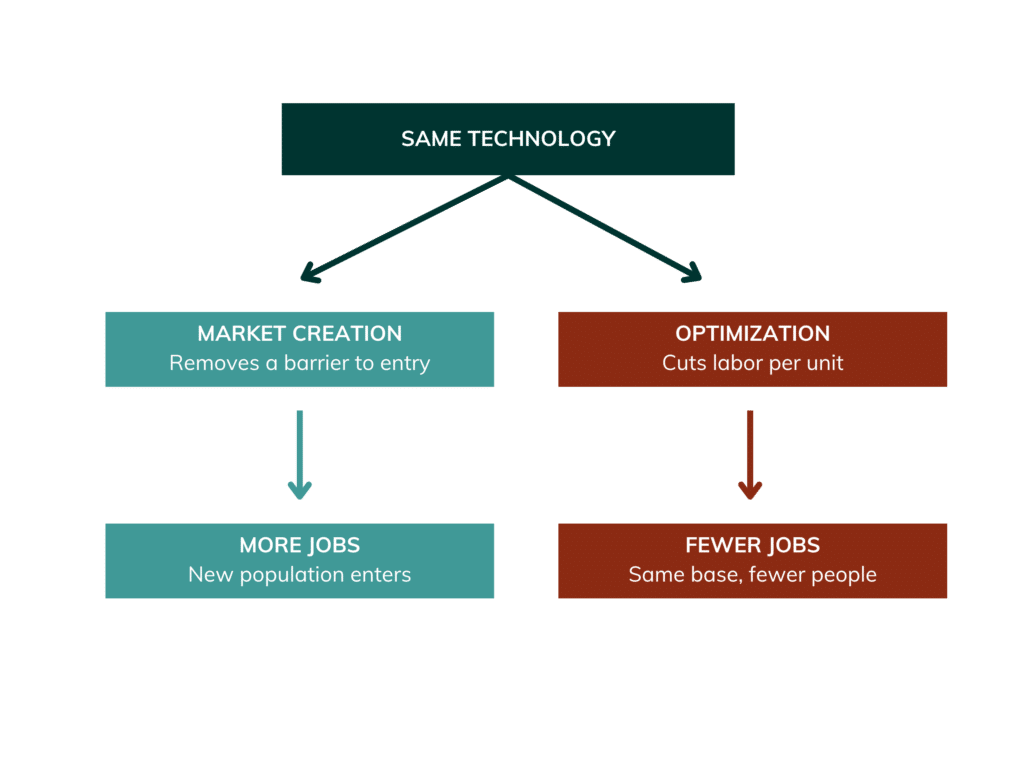

To understand when productivity leads to market expansion and when it leads to labor substitution, the most useful distinction isn’t in the technology itself, but in how it’s used. Christensen’s framework, particularly as developed in his book with Efosa Ojomo, The Prosperity Paradox, lays out two directions, and employment follows each almost mechanically.

The first direction is enabling a new population to enter the market by removing a barrier that kept them out: cost, knowledge, capital, physical access, or regulation. Christensen and Ojomo call these absentees “nonconsumers.” When the barrier falls, new people come in, and the market expands because the absentees arrive, not because existing customers consume more.

The second direction is to serve the same customers, offering what they already value, only at a lower cost or more efficiently. The productivity gain comes from reducing the amount of human labor per unit. The customer base doesn’t change, but the number of people needed to serve it does.

Both directions are legitimate strategies, and healthy companies do both. The point is not which is better. It’s which produces which effect on employment.

But there is an asymmetry behind that choice. Nonconsumption is structurally invisible. Market research measures who responds. Sales spreadsheets measure who buys. The P&L measures who pays. Whoever sits outside the market shows up nowhere. The first direction requires seeing a population that the management system wasn’t built to see, and so the natural bias of companies is the second direction.

Nubank and the incumbents are in the same industry

Financial services show the two directions running in parallel, within the same industry, on top of the same underlying technology. On one side are Nubank, PagBank, Banco Inter, and Mercado Pago. The technical stack isn’t different from that of the large banks: ML for credit risk, mobile-first apps, automated decisioning, and API-based integration.

What changed was who became a customer. Nubank reached more than 100 million people, and for many, it was their first credit card or their first formal banking relationship. The barrier that fell was the one that defined who the system considered “serviceable,” and when it fell, new people entered.

And it wasn’t just new customers. The strategy also pulled into the country data centers, engineering teams, venture capital, and new relationships with regulators. That’s institutional infrastructure that normally takes decades to form.

On the other side is the same technology, only applied to automating back-office operations, credit analysis, customer service, and operations at traditional banks. The customers are largely the same, and so are the operations. What changes is the human labor per operation processed, which falls. Itaú, Bradesco, and Santander together account for tens of thousands of layoffs over the past decade, and thousands of branches have been closed. It’s the same underlying technology, in the same sector, with two different uses producing opposite effects on employment at the same time and in the same country.

These examples help raise three questions to separate the two directions in front of any new application of AI:

- Is there a population that couldn’t participate in this market but can now because a barrier has fallen?

- Is the customer base substantially the same as before?

- Is the value in enabling new participants, or in doing the same work with fewer people?

Cut or create

Look at AI today, and the landscape is clear: automated customer service, content generation at an industrial scale, and code copilots aimed at reducing the need for junior hires. All of it serves customers who were already being served and does work that was already being done. The barrier that fell was the company’s cost.

Now look at the other side. The small exporter who could never afford a translator now negotiates directly with a Chinese supplier. Whoever never had access to a private tutor now does, and whoever couldn’t afford a legal consultation now gets oriented. The same applies to a designer or personal analyst.

The solo founder runs a company that, five years ago, would have required 10 people. In each of these cases, the population that participates now wasn’t there before. They’re the same models, the same API, the same underlying capability, and what changes the direction is how the technology is being used.

Both directions are real, but they don’t run on the same scale. Most current use of AI is focused on cost reduction, which is hardly surprising. With any general-purpose technology, cost-cutting arrives before new market creation. The steam engine spent decades eliminating work in mills before the railroad pulled entire populations into paid labor.

AI can follow the same arc, or it can fail to do so, because the arc isn’t automatic. It depends on the choices of whoever is building, funding, and using AI right now, including yours, and those choices, summed at scale, shape the labor market of a generation.

Stop asking whether AI will destroy jobs. Start asking what each of us is doing with it.