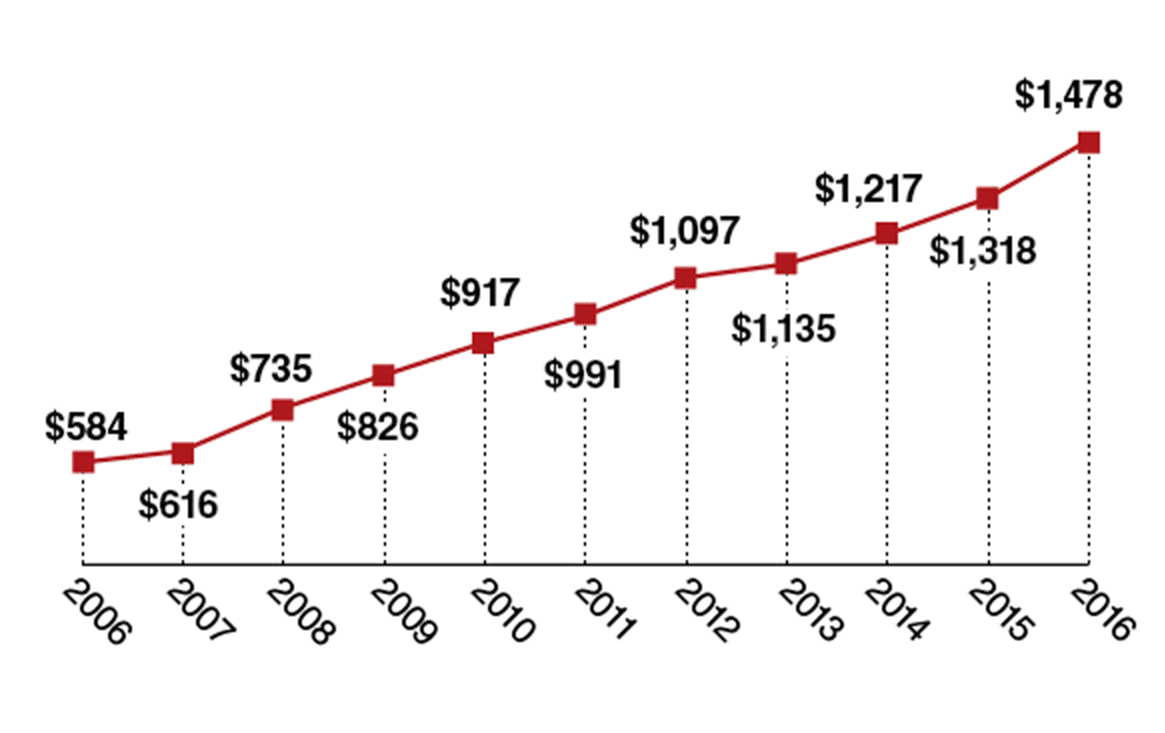

Since the open enrollment in the health exchanges under the Affordable Care Act (ACA) began in late 2013, the percentage of American adults without health insurance has fallen from 18% to 9%, the lowest rate ever recorded. Despite such a positive trend, the average cost burden for single workers continues to increase (Figure 1). Given that more than 20 million newly insured have now begun paying health insurance premiums, it is puzzling why the average cost burden has not fallen, but risen—between 2015 and 2016, individual premiums paid to employers have gone up 3% while personal deductibles have gone up 12%.

Several factors might contribute to this trend of increasing burden. It is possible that many of the beneficiaries of the ACA exchanges have multiple health issues that are adding new costs to the system. Major private insurance companies exiting the exchanges after incurring heavy losses point to this possibility. It is also possible that the prices of healthcare products and services have gone up over the same period. Since 2013, revenues of the major private insurance companies have grown more than 10% per year, but their costs have similarly increased. While the ACA has been successful at creating a safety net for millions of previously uninsured, it has yet to address the total costs of America’s health system and financial burden on individuals.

Clayton Christensen, the co-founder of the Christensen Institute and architect of the theory of disruptive innovation, explains that the current situation in America’s healthcare is exactly where disruptive innovations will emerge. Disruptive innovations target those customers who are either not consuming or consuming very little of existing products or services. Despite the rise in the size of the insured population, high insurance deductibles are causing people to forgo seeking needed care, making them the perfect target for disruptive innovations. To that end, we offer three ideas that innovators can implement to reduce the cost burden for the insured.

Figure 1: Average Deductible for a Single Worker with a Deductible Plan

Sources: Kaiser Family Foundation/HRET; Modern Healthcare

1. Target growing deductibles

Because insurance deductibles have become unaffordable for many, more consumers are reluctant to seek needed care. This growing trend in nonconsumption only leads to more costly health problems when major issues are discovered late in the game. Innovators need to come up with simple, value-adding products and services that consumers can easily purchase out of pocket. Retail clinics, for example, could play a significant role in bringing high-value health services to an increasing number of nonconsumers who have some financial means but are unable to cover their deductibles.

2. Manage risks and patients

The current insurance model has not been able to prevent rising costs of care, especially for those with complex health problems. What the past two years of the ACA exchange have shown is that private insurance companies are so busy looking for ways to distribute the cost burden of less healthy patients across healthier members, that they’ve lost cost control at the individual level. As this sharing of risk across the insured population has failed to reduce costs, insurers have responded by fleeing the exchanges. Fortunately, this might be a great opportunity for disruptors who could promote healthier behaviors and lifestyle through incentive programs. As some of the emerging business models such as Iora Health and OnPointe suggest, proactively managing individuals’ health conditions by rewarding healthy behaviors could result in improved patient compliance and more timely delivery of care, two of the main sources of inefficiency in current healthcare.

Moreover, such health management solutions could offer a viable insurance model in markets where other insurers have failed. Already, major health organizations such as American Cancer Society (ACS), American Diabetes Association (ADA), and American Heart Association (AHA) have proposed financial incentives to encourage healthy behaviors. Although there is much debate around the issue of rewarding behaviors, these models at least reduce health costs for those who use the system less and encourage behavioral changes for others that will further drive health costs down.

3. Focus on consumer healthcare products

Innovations within the current healthcare environment (FDA approved products) tend to raise costs, because they are mostly sustaining innovations that focus on improving performance of existing solutions at higher prices. As we have alluded to in the past, the healthcare industry has little incentive to offer a product or a service that is less expensive than the status quo. Therefore, the job is left to those outside of healthcare to bring innovations that will fundamentally change how healthcare products and services are viewed and consumed. As an example, a recent comment by a physician hired by Apple has caught our attention. Dr. Mike Evans at Apple predicts that in the near future, an app will be able to help users adopt a healthier lifestyle and comply to treatment regimens from physicians. If these apps could be perfected, they could serve as affordable tools to deal with difficult-to-treat patients who need greater supervision and management.

The current reimbursement model is largely based on actuarial risk models using population statistics. Such large population-based models tend to overlook individual variations and differences, essentially discounting lower-risk factors at the individual level while amplifying risks at the population level. We need a reimbursement model that rewards individual success and improvements, but the current reimbursement community, including the government, seems to be too focused on sustaining their existing business models. It’s time for innovators to disrupt the establishment.