Oberlin College, in Oberlin, Ohio, boasts a nearly $800 million endowment and is ranked 26th by US News & World Report. And if you are lucky enough to be admitted to the highly selective school, tuition, room, and board can be yours for just a hair under $70,000 per year.

Despite what may, at first blush, seem like an elite school with oodles of wealth, Oberlin is in financial straits. Understanding why reveals broader cracks in the business model of higher education, and that elite schools can be among the most vulnerable.

Running at Full Capacity

Matching supply and demand is a tough problem in any industry. Companies typically have a variety of levers they can push: raising or lowering prices, increasing production, or reducing supply.

But residential liberal arts colleges are constrained from pressing on many of these levers, reducing their flexibility to adapt to changing conditions. For starters, the residential, people-intensive nature of the experience means that supply—the number of seats in the class—is relatively fixed. These colleges can’t build more dorms on a moments notice. And they will be dinged in the rankings for expanding number of students in an average classroom.

Enrolling fewer than the targeted number of students is an even worse outcome. Enrollment shortfalls lead to revenue shortfalls, which require budget cuts—and budget cuts are very unpalatable at elite schools for a number of reasons. First, many of the the costs, including significant facilities and maintenance expenses, are fixed. Professors are tenured, limiting colleges’ ability to hire and fire. And professors at elite schools tend to be fairly competitive on the job market—they have plenty of other options if schools can’t match the salary increases of peer institutions.

Oberlin’s numbers show just how razor thin the margin of success or failure can be in the world of elite liberal arts schools. In the 2017-18 school year, Oberlin targeted a total student body of 2,895, and ended up with total enrollment of 2,815, falling short by 2.8%. But that shortfall led to a $5 million budget gap, two years of salary freezes, the elimination of faculty research grants, and a college-wide search for more fat than can be cut.

The Treadmill of Sustaining Innovation

In the short term, budget cuts are the only solution to Oberlin’s woes. But in the long term, they may worsen the school’s fiscal position. Cutting spending can lead to a death-spiral of reduced student demand that requires even more cuts.

In most industries, the competitive dynamic is dominated by sustaining innovation: innovations that make good products better, and more appealing to an organization’s best customers. This is true in higher education, in which the pursuit of prestige dominates decision-making. Schools spend millions on the pursuit of full-pay students, and a facilities arms race threatens to destabilizes the finances of the sector. In a hyper-competitive market, schools cut costs at their peril.

In quantitative terms, cutting spending can lead to hits in the rankings. Spending (per student) constitutes 10% of the US News ranking methodology. But news of a school firing professors or cutting research spending can also ripple through the higher education community—and a peer assessment of reputation counts for another 15%. Faculty salaries are another 7%.

But qualitatively, cutting spending on almost anything that could be visible to a prospective student could result in lower admissions numbers. High-income students who can pay full tuition matter a great deal to a college’s bottom line. Losing even a handful can create a big budget impact, and lower selectivity numbers hurt the rankings too.

The treadmill of sustaining innovation creates pressure to find new revenue sources, rather than cut costs, and indeed, this is what Oberlin’s leaders have decided to do. Despite sky-high tuition, leadership has concluded that the school’s issues stem from tuition revenues that are too low. There simply aren’t enough students who are willing and able to pay the prices that schools are charging.But the prestige-based nature of higher ed competition means that lowering costs and prices is a dangerous last resort.

Value Proposition Crumbling

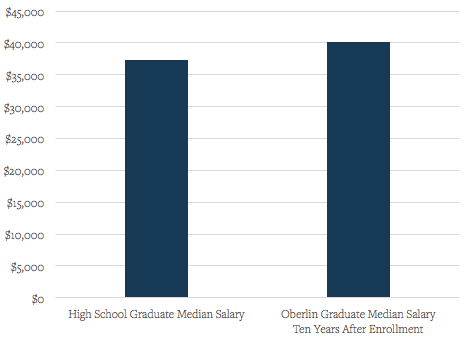

Input-driven rankings like US News & World Report put Oberlin near the top of the pack. But the Economist, which ranks schools based on outcomes, puts Oberlin 964th out of 1,275 schools. In ranking Oberlin near the bottom, the Economist’s methodology compared the salaries of alumni ten years after enrollment with what those graduates would have been “expected” to earn given their demographic information, including SAT scores and zip codes. In this analysis, Oberlin students ended up earning $2,368 less than their demographic data would otherwise predict.

A Vulnerable Model

Higher education is diverse: Oberlin’s business model is dramatically different from that of a public institution or a career college. But Oberlin’s travails illustrate the challenges faced by other small-private-residential-liberal arts schools, even at the elite level.

The business model offers little flexibility for coping with a changing landscape. The imperative for increasing revenues—and spending—is so unbelievably strong that schools like Oberlin are beginning to price themselves out of the market. And the value proposition isn’t holding up against the massive costs families are being asked to pay.

We write a great deal about the potential of Disruptive Innovation to upend higher education. But even in a world without looming disruption, the higher education business model is in danger of collapsing under its own weight.