In my “Industry Disruption & Corporate Transformation” course at Northeastern University, Netflix is arguably the best example—and certainly the most popular with students—of disruptive business strategy. Students can practically recite the Netflix origin story by heart (even though they weren’t yet born!): how a scrappy DVD-by-mail service disrupted, and ultimately took down, Blockbuster—the 800-pound gorilla of video rentals.

Early Netflix is a textbook case of Disruptive Innovation, and a popular case study for the students who are enthusiastic customers. But as I begin to teach this course again this semester, I’ve realized that the historic Netflix story I’ve been teaching bears little resemblance to the Netflix of today.

We’re currently witnessing the opening bell of “Chapter 3” of the Netflix story. With Netflix lined up to acquire the assets of Warner Bros. Discovery (WBD), we aren’t just looking at another media merger. We’re looking at a high-stakes test of Clayton Christensen’s “New M&A Playbook.”

The question for Netflix is no longer how to disrupt an industry, but how to manage incumbency while continuing to innovate and lead.

The three chapters of Netflix

To understand the weight of the WBD acquisition, we have to look at how Netflix has evolved over three eras:

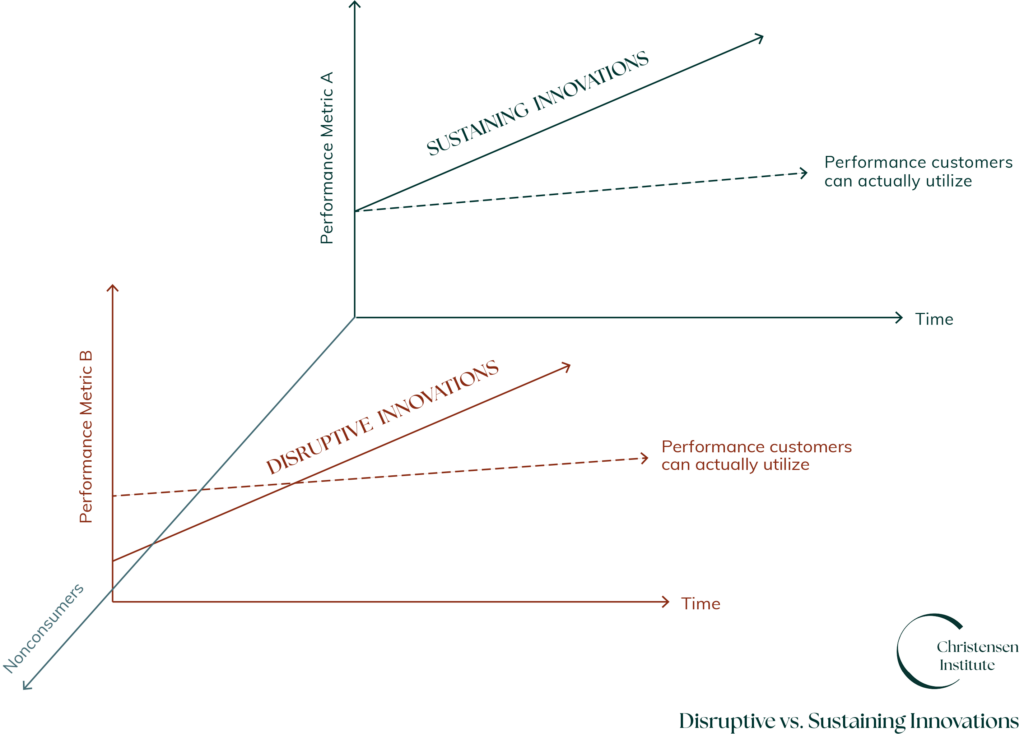

- Chapter 1: Disruptive Innovation (The Blockbuster Era). Netflix entered the market with an initially inferior product (you had to wait days for a DVD) that appealed to an underserved segment: cinephiles looking for a deeper catalog of less common titles (e.g., the “long tail”). Netflix used a simple, low-end channel (physical mail) to bypass the high fixed costs of video stores.

- Chapter 2: Sustaining Innovation (The Streaming Wars). As Netflix moved upmarket into streaming, it became the benchmark. It’s important to remember that Netflix effectively disrupted its own DVD-delivery business to lead the streaming industry (for those who remember Qwikster). Streaming quickly became the dominant design for consumer media consumption. As this happened, the competitive battle shifted from distribution to content, and this Netflix era was defined by numerous sustaining innovations—improving the interface, expanding their library, increasing video quality, and adding features such as gaming and podcasts —all while spending billions on original content to keep ahead of competitors such as Disney+, Amazon Prime, and of course HBO Max.

- Chapter 3: Business Model Reinvention (The M&A Era). Today, streaming has clearly become the status quo to a point where many are questioning whether even traditional cinemas have a future. Industry growth has plateaued because there are few new or untapped customers to add, while margins compress amid numerous competing services and content costs spiraling ever upward. In this environment, a potential merger with a legacy giant like Warner Bros. Discovery suggests Netflix is seeking a new playbook.

The new M&A playbook: Resources vs. business models

According to “The New M&A Playbook”, there are two fundamental reasons to buy a company. You either buy it to bolster your current business model (a “resources” play) or you buy it to develop a new business model (a “reinvention” play).

If Netflix acquires WBD simply for its library—assets such as Harry Potter, DC Comics, and HBO library —they’re making a traditional resource play. They are betting that more content will make their current subscription model more “sticky.” Publicly at least, that has been their acquisition pitch thus far.

However, if Netflix is looking at WBD’s linear assets, its advertising infrastructure, and its diverse theatrical distribution as a way to fundamentally change how they capture value, they could attempt a trickier—but potentially more powerful—business model reinvention. Competing bidder Paramount appears to be following this strategy, and using it (thus far unsuccessfully) to convince WBD shareholders that it offers a better long-term deal.

While the resources path is, at least in the near term, less risky for Netflix, it may also be more limiting in the long term. Large companies frequently fail with M&A because they try to force a newly acquired business into their old way of doing things; in other words, they “integrate” the life out of the acquisition. For Netflix to succeed in Round 3, they may have to consider something counterintuitive: keep the legacy media “messiness” of Warner Bros. separate enough to let it transform them. Ironically, the competing bid from Paramount may force them to do exactly that, since Paramount is explicitly (perhaps out of necessity) taking more of a reinvention approach.

When disruption becomes the status quo

Netflix provides a prime example of what Christensen called the “Innovator’s Dilemma”: as companies succeed, the management practices that made them successful can often lead to their eventual downfall over time.

For years, Netflix’s “North Star” was simple: no ads, no live sports, and “all episodes at once.” One by one, those pillars have fallen. They’ve successfully introduced an ad-supported tier, experimented with live events like NFL games and boxing, and are continually refining release schedules for their ever-expanding content library.

These aren’t just “features.” They are signals that the original disruptive model of pure-play subscription video is no longer enough to sustain the company’s growth and take the business to the next level.

When a company begins to acquire its older, “dinosaur” competitors, it’s often a sign that the industry has reached the “Transitional Phase” of its industry lifecycle. The fluid, experimental days are over. Consolidation is the name of the game.

Why this matters beyond Hollywood

The Netflix/WBD saga is a bellwether for every disruptor from the last twenty years. Whether it’s Uber, Airbnb, or Tesla, companies all eventually face similar “Chapter 3” dilemmas.

When your original disruptive advantage becomes the new status quo, you can’t just innovate “better” versions of your current product. You have to decide if you are willing to disrupt yourself—even if that means acquiring the very incumbents you once sought to replace, and radically changing the business model that got you to the pinnacle—before you get knocked off of it.

As I discuss with my students, disruption happens within industries, but transformation happens within organizations. Netflix has proven it can do the former. Chapter 3 will demonstrate how well they can pull off the latter.