High-deductible insurance and health savings accounts (HDI/HSA) are on the rise. Industry experts forecast that 4 out of 5 large employers will offer their employees HDI/HSA coupled plans in 2015.

The increase in average deductibles represents a worrisome cost to some Americans, many of whom are unable to afford needed health care services. Rising health care prices and fewer patients seeking care reinforce these concerns.

These trends will likely heat up the debate about patient safety and runaway costs in health care. Is the HDI/HSA model part of the problem? Or part of the solution?

In effect, the HDI trend means employers are transferring more of the direct cost of care to their employees. And in the absence of the employer HSA contribution, high deductibles could induce pressure not to consume needed care. But as long as the HSA value equals the deductible, the HDI/HSA model will effectively shield consumers from high costs in the short term, making it roughly as effective at “coverage” as traditional insurance.

Disruptive innovation theory suggests that adoption of the HDI/HSA model could be an important move towards making health care more accessible and cheaper. This is largely because the HDI/HSA model is actually a much better fit than the traditional coverage model to meet patients’ “jobs to be done.”

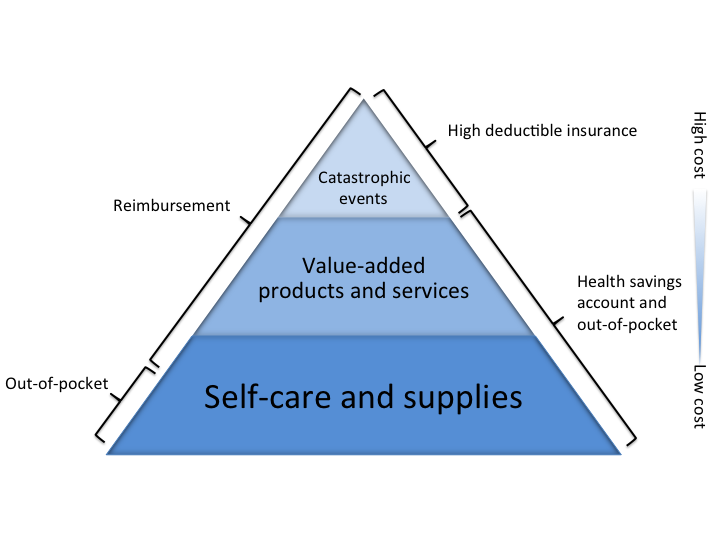

The consumer’s health care “jobs” can be segmented into three general categories:

- coverage for catastrophic events

- value-added products and services

- self-care and supplies

From the patient perspective, catastrophic events can be devastating because they are both unexpected and very high-cost. The insurance model works well to spread the risk of these events over a larger population and shield individuals from their full financial effects.

Patients seek value-added care services when the need is relatively predicable, but the patients cannot do it for themselves. These are services such as minor procedures, monitoring, and care for chronic conditions. Finally, self-care and supplies are regular health care needs patients address themselves, sometimes every day, such as brushing their teeth or purchasing Tylenol.

The traditional model of health insurance—the indemnity model—is well suited to the job of paying for catastrophic events. It has been successfully applied to diverse needs like auto or home coverage and works for catastrophic events in health care too. But the other two jobs are not well served by this model: the difficulty of making timely doctor’s appointments, the surprisingly high price tags of simple procedures or office visits, and costly medical supplies are among the inefficiencies of the current model. In many cases, these needs can be met much more quickly, and by lower-cost options—that is, when individuals have more control and choice in managing their care.

Consider a patient who gets a routine blood test order from her physician. If she has traditional insurance coverage, she might just go to the hospital lab, overlook the long wait time and enjoy the $5 copay. Only her employer or insurer sees the true price of these labs. But as a patient with an HDI/HSA plan, she gets billed the full amount—and it quickly turns into hundreds. Incentivized to find a lower cost, more convenient solution, she hops online and finds a local Walgreens with a Theranos blood testing lab. The total comes to $25—and she can use her HSA dollars to pay for it. True, she had to shop around a little, but the test was way cheaper, less painful and the results were sent to her smartphone.

Which would you choose?

This is the strength of the HDI/HSA model: it can empower consumers to choose low cost, efficient solutions to their problems in a competitive market. It has the potential to put newfound HSA dollars towards business models optimized to meet the non-catastrophic health care jobs that consumers regularly experience.

For a number of reasons, the benefits of the HDI/HSA model have been slow to materialize in practice. But the rapid adoption of this new payment model suggests the climate is becoming more favorable for the emergence of much-needed affordable, new market disruption.