Devin Bean, a research assistant at the Clayton Christensen Institute, and I coauthored this piece. It is based on a report by the Clayton Christensen Institute titled, “Seize the ACA: The Innovator’s Guide to the Affordable Care Act.”

Since its passage in 2010, the Patient Protection and Affordable Care Act (ACA) has been analyzed by experts from nearly every political, economic, and health policy angle possible. Yet in the noisy debate about whether the legislation is good or bad and whether to implement or repeal it, we think there’s something missing: a rigorous but practical discussion of the innovation opportunities created by the legislation and the barriers to innovation it imposes.

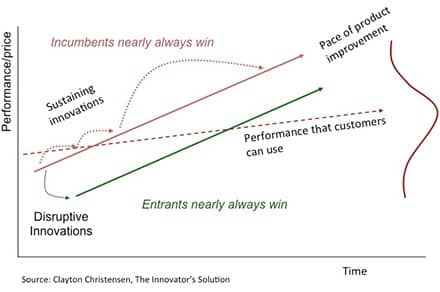

To facilitate that goal, we analyzed the ACA through the lens of the theory of disruptive innovation. First articulated by Harvard professor Clayton M. Christensen, disruptive innovation theory explains how innovations that decrease cost and increase accessibility transform entire industries. As existing products increase in performance and begin to exceed customer needs (think of next year’s biggest Cadillac model), low-cost, lower-performance alternatives created by new entrants take root in the low end of the market (think of next year’s smallest Kia model). These new products are initially inferior in comparison to established products, but they become better and better until they “disrupt” and eventually topple larger incumbent competitors.

So how does the ACA affect the pace of disruptive innovation in health care? What opportunities does it create for innovators? What barriers does it inadvertently erect? Here are a few thoughts from our recent paper.

ACA provisions that encourage disruptive innovation

- Individual mandate

- The individual mandate requires every person to carry health insurance. The influx of previously uninsured patients will overwhelm the current primary care system, likely creating the need for new disruptive care delivery models at the low end of the market.

- Employer mandate

- The employer mandate requires all employers with 50 or more full-time employees to offer health insurance benefits. Due to the specific form of the penalties for not providing insurance, this provision creates incentives for employers to disaggregate true insurance from routine reimbursement and manage day-to-day care. Employers will have opportunities to disruptively integrate around employees’ health care needs.

ACA provisions that discourage disruptive innovation

- Essential health benefits

- This provision requires all health care plans to provide, at a minimum, a package that includes access to certain types of care and services. This provision discourages disruptive innovation by essentially establishing a floor on the low end of the market, making it even more difficult for disruptive entrants to gain market share.

- Insurance exchanges

- These online insurance marketplaces are themselves a disruption-neutral idea. The regulations that accompany the exchanges, however, are barriers to disruptive innovation. By mandating health plan actuarial values and forcing insurance providers to offer plans at Silver and Gold levels, the exchanges force new entrants to compete against incumbents and put a value floor on the market that discourages innovation.

None of these provisions will transform healthcare, for better or for worse, on their own. Although some of the provisions of the ACA may open doors for disruptive innovation, the onus rests upon the health care sector—existing players and new innovators alike—to seize the disruption opportunities and create products and services that make health care more affordable and accessible.

Despite the vitriol about the ACA, one objective nearly everyone can agree on is that health care in the United States needs to become more affordable and accessible without compromising quality. For that to happen it is crucial for innovators and policymakers to understand and seize the disruption opportunities presented by the ACA and navigate around the barriers imposed by it. In this way we are convinced brilliant individuals and companies can innovate within the framework of the ACA to make care more affordable and accessible for all.