{kind=link}

Insurers construct deductibles into their health plans as tools to prevent members from spending more on healthcare than they truly need. They reason that if members have ‘skin in the game,’ they will prudently shop around for reasonably priced healthcare providers, and not purchase more healthcare goods and services than necessary.

Regardless of whether or not this tactic encourages wiser healthcare purchase decisions, prices for healthcare goods and services keep rising at such a rate that shopping for the best bargain has become a penny-wise and pound-foolish task for consumers. In other words, the amount that healthcare consumers can save by tediously bargain shopping for the best price pales in comparison to the actual cost of the service. Furthermore, individuals are not well equipped with the healthcare knowledge and price information necessary to make informed purchasing decisions in most situations. Thus, health insurers should not force their members to struggle in choosing between any number of high-priced options, but should proactively expand their scope to lower-cost spaces outside of the traditional healthcare system to help their members manage the risk of major health issues and potentially prevent devastating healthcare expenditures in the first place. In doing so, insurers could potentially bear less risk when insuring their members by empowering them with tools to help maintain their health and wellness. This is an important distinction, as it’s everyday individuals who will have to play the defining role in curbing the continued growth of healthcare costs, by ultimately leading healthier lives.

Rethinking the deductible

Insurers are in an excellent position to actually use rising deductibles as a tool to motivate members to purchase health promoting goods and services. Health insurers could effectively lower members’ deductibles when they decide to make health-promoting purchases, by deducting the total (or a percentage of the total) purchase of pre-approved products or services from the member’s deductible. These types of products would include Fitbits, health club memberships, and meal plan purchases for those with dietary restrictions from companies like Blue Apron, Plated, or Jenny Craig.

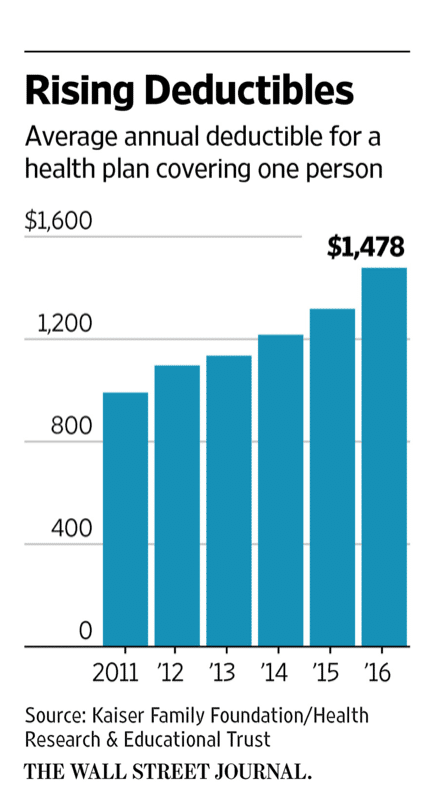

For example, consider Sandy, who was recently enrolled in a high deductible health plan through her new employer with a deductible of $2,000 dollars. She has a condition that requires regular check-ups, compliance with a prescription medication regimen, a controlled diet, and maintenance of a certain level of activity. Despite being insured, she still has to pay $2,000 before her plan begins to fulfill the reason it was purchased in the first place.

Imagine if she were able to deduct the purchase of an activity-tracking device like a Fitbit and personalized meal plans from a meal and ingredient delivery service like Blue Apron from her $2,000 deductible. She would be better equipped with the tools necessary to be in compliance with the activity and dietary aspects of her health and wellness regimen, and in the meantime, she could end up cutting her deductible almost in half over the course of ten weeks. A lower deductible would then put her in a better financial position to save money on her doctor visits and prescription medications with actual assistance on her healthcare bills.

In the case of Sandy, and countless other Americans, the deductible deduction would give individuals an additional nudge to purchase products that can make it easier for them to maintain or improve their health. This motivation is greatest for those members who have a high deductible, and regularly meet their plan’s deductible each cycle. Even typical nonconsumers of healthcare would have added incentive to improve their health plan product and effectively lower their plan’s deductible. By decreasing the amount members must contribute before helping them with payments, insurers would be more likely to assist with the truly expensive burden of traditional healthcare costs—the reason the insurance was purchased in the first place.

Managing Risk

For insurers, deducting these purchases from a plan’s deductible is a lower-risk way of empowering health maintenance among their membership compared to covering these goods and services outright. This lower risk stems from the fact that not all members who take advantage of this feature will end up meeting their health plan’s deductible. In these instances the insurer does not end up spending more than they would have had they not offered the deduction, but their member is still better equipped with tools to manage their health. Thus, the deductible enables insurers to test which proactive health interventions improve health status in a cost-effective manner and which don’t. After aggregating evidence from the deductible arena, insurers can add even more value to their members’ health plans by reimbursing members for select interventions proven to improve member health and lower overall healthcare expenditures. These types of coverage benefits are already prevalent in select high-end health plans who cover gym memberships among other products and services (see Aetna’s coverage of Apple’s iWatch).

Leveling the playing field

It is also possible that widespread adoption of such policies could motivate innovation and entrepreneurship efforts in the health and wellness industry, which is a trend from which everyone could stand to benefit.

By giving those with high deductibles a constructive way to lower their deductibles, deductible deductions can play a role in reducing social and economic inequities between those with lower-quality health plan products and those with superior ones. These deductions can reverse the role of the deductible from compelling plan members to futilely pinch pennies when purchasing healthcare services, to encouraging the purchase of products that empower health and wellness.

This piece was originally published on The Health Care Blog.